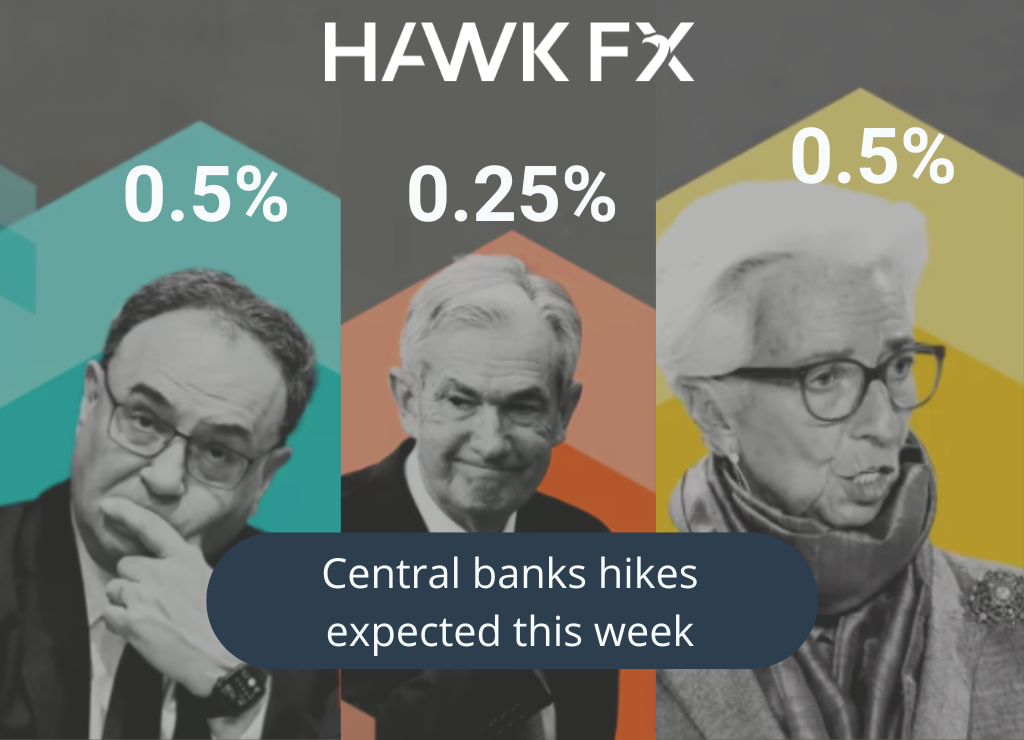

This week the big questions will be answered by three major central banks regarding how much they will hike rates. The Bank of England is widely expected to raise rates by 0.5% again to 4%. The majority of the panel will likely point to inflation risks. Although inflation will continue to fall, inflation in the services sector has been stickier and may keep the BoE raising rates into the second quarter. A couple of MPC members (Dhingra and Tenreyro) are likely to vote against a hike again, and markets will be watching to see whether there is any further diverging of views from the panel.

Last week we saw further weakness in the economy, with the composite PMI for January coming in at 47.8, signalling contraction at the start of the year. We also saw producer price inflation figures continue to fall, with the rise in prices down to 16.5%, from the peak of 24.6%. The indices of future output are improving. With the data showing a weakening economic picture, it seems to be a matter of time before the Bank of England starts to moderate their rate hikes.

With the amount of data and central bank decisions this week, we could see an increase in volatility this week. A key question will be whether the central banks make any changes to their communications to suggest that interest rates are close to their peak. Last week, we saw the Bank of Canada only raise interest rates by 0.25% to 4.5% and indicate that it will now pause. This week, we don’t expect a similar approach from any of the central banks, given the uncertain economic outlook, it is likely that policy moves will remain data dependent.

GBPEUR – 1.1409

GBPUSD – 1.2393

The European Central Bank follows the Bank of England decision on Thursday. The market expectations are for another 0.5% hike, raising the deposit rate to 2.5%. President Lagarde has already suggested that this is the likely outcome and will be supported by data that suggests the economic downturn is likely to be shallower. Although Eurozone inflation has started to fall, policymakers remain concerned that core inflation is still rising. Given this situation, markets expect further hikes through to the second quarter.

Ahead of the ECB policy decision, we will see the first estimates of fourth-quarter GDP as well as the ‘flash’ January CPI estimate. Recent PMI surveys suggest that the Eurozone economy is holding up better than expected, helped by lower energy prices. We expected a marginal contraction of 0.1% in the fourth quarter, which may see the Eurozone avoid a technical recession, for now at least. The inflation figures are also expected to fall due to lower energy prices. We expect CPI to fall to 8.8%, mainly due to lower energy prices. We also expect core inflation to edge lower from 5.2% to 5.0%, which would be the first fall in over six months.

EURUSD – 1.0862

EURGBP – 0.8765

The Federal Reserve will be the first central bank to publish its decision this week, on Wednesday. The Fed is expected to hike rates by a smaller 0.25% to 4.75% this month. This would follow hikes of 0.75% in November and 0.5% in December. Markets are not expecting the Fed to call for a pause as the Bank of Canada did last week, but it is possible that they will pause at the next meeting. There is no update of the ‘dot plot’ this month, which shows Fed policymakers’ interest rate expectations. The latest one in December suggest interest rates could be above 5% by the end of the year. Markets will be looking for further hints in the post-meeting comments, on expectations for short-term hikes, but also for longer-term cuts in rates.

We will end the week with further data from the labour report. There have been reports of job losses in the tech and other sectors. These announcements of cuts have not shown up in the labour market reports so far. Markets expect the nonfarm payrolls to post another strong rise of 200k. The unemployment rate will likely be unchanged at 3.5%. The employment cost index will also be closely watched, after falling last month. Earnings growth is expected to fall to 4.4%, which adds to a picture of falling inflation pressures. This has also raised hopes of the potential for a soft landing, with GDP rising by 2.9% in the final quarter of 2022.

GBPUSD – 1.2393

EURUSD – 1.0862

Do get in touch if you would like to discuss this further.

*Interbank rates correct at 7 am on the date of publishing.